The Independent Governance Committee (IGC) was founded by ReAssure in 2015 to review the value for money provided by ReAssure workplace personal pension schemes. ReAssure also has two trustee boards, which you can find out more about below.

Welcome to this year’s annual report from the IGC

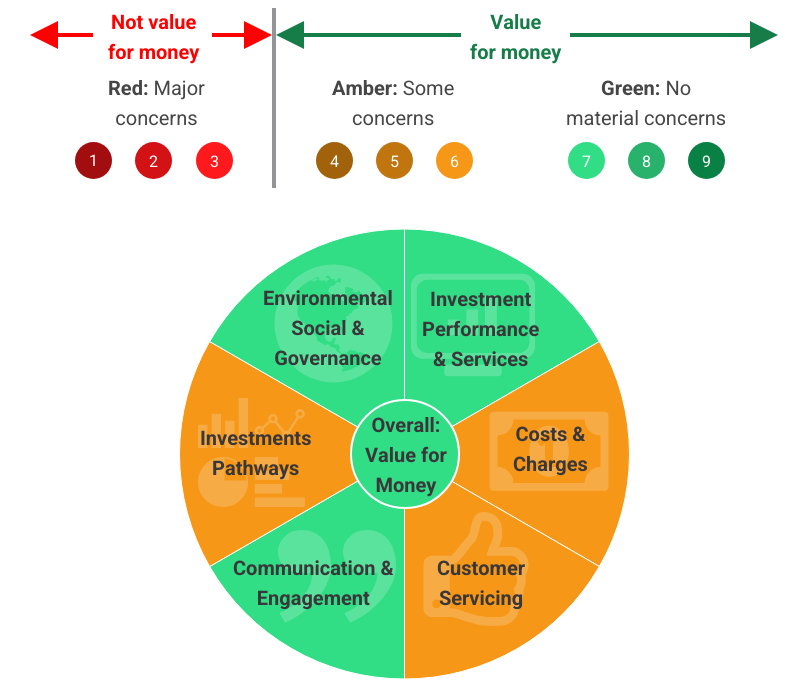

The IGC independently assesses whether customers are receiving value from ReAssure. We review the products and services they offer and challenge them to make improvements where needed. We consider a range of areas including investment performance, costs and charges, customer servicing, the quality of communications, investment pathways and Environmental, Social & Governance (ESG) factors.

The IGC independently assesses whether customers are receiving value from ReAssure. We review the products and services they offer and challenge them to make improvements where needed. We consider a range of areas including investment performance, costs and charges, customer servicing, the quality of communications, investment pathways and Environmental, Social & Governance (ESG) factors.

Each year we report our findings. Below is a summary of where we believe value is being delivered and where improvements can be made. You can also download the full 2024 report for further details.

“Our view is that you are receiving value for money”

We assess each of the areas to determine if Red (not value for money), Amber (value for money but could be improved), or Green (value for money). We also decide if they are low, medium or high within each category. This results in a final rating between 1 and 9.

You can click the boxes below to find out more information about each area.

Investment Pathways

Costs and Charges

Customer Servicing

Communications and Engagement

Environmental, Social & Governance

Investment Performance & Services

Read the full report and how we made our assessment that ReAssure offers value for money

Download the full 2024 report

Download the supporting material

Costs and charges

It’s important that you consider the costs and charges you pay for the ongoing administration of your workplace pension. On this page, you can find tables showing the range of costs and charges paid by members who invest in all funds offered by ReAssure, along with some sample illustrations showing how these charges could affect the future value of your pension.

Meet the board members

Andy joined the IGC as an independent member in September 2023 and was appointed as the Chair in January 2025.

Andy joined the IGC as an independent member in September 2023 and was appointed as the Chair in January 2025.

Andy is an experienced strategist, marketer, and business development professional with a strong customer focus. His career of over 35 years spans the breadth of Financial Services covering pensions, wealth management, life, healthcare, and general insurance. He has held a wide range of senior management positions including Director of Marketing Strategy & Customer Insight for AXA UK & Ireland during which he established their first customer centricity strategy. Whilst Head of Strategic Development for AXA Life, Andy created the initial strategy, and was one of the founder members of the Elevate investment platform (now Aberdeen Elevate).

Andy is also an independent non-executive trustee for the Standard Life Master Trust Co Ltd. He also runs his own management consultancy business specialising in strategic change and business transformation and chairs a business ‘Mastermind’ group of leaders of small/medium businesses in the Southwest.

Andy has qualified as a Chartered Insurer and Financial Planner in addition to holding separate professional Project, Process and Proposal Management qualifications and is an Accredited Professional Trustee with the Pensions Management Institute.

Rachel joined the IGC as an independent member in August 2022. She is a customer-focussed leader with extensive experience in the financial services industry, including Marketing and Digital roles within HSBC First Direct and Product, Proposition and Customer Experience Director for Coventry Building Society. Rachel’s expertise spans strategy, marketing, digital transformation, risk management and cultural leadership. She holds a number of other non-executive roles within the financial services, currently as a Non-Executive Director and Chair of Remuneration Committee for both Mansfield Building Society and the Mortgage Advice Bureau. Rachel has a personal passion for ensuring customers are treated fairly and is particularly keen to make sure consumers, including those considered vulnerable, get value for money and good outcomes from their pension decisions. Rachel’s wide-ranging experiences will help the IGC build on its assessment of the value offered in both retirement products and investment pathways.

Rachel joined the IGC as an independent member in August 2022. She is a customer-focussed leader with extensive experience in the financial services industry, including Marketing and Digital roles within HSBC First Direct and Product, Proposition and Customer Experience Director for Coventry Building Society. Rachel’s expertise spans strategy, marketing, digital transformation, risk management and cultural leadership. She holds a number of other non-executive roles within the financial services, currently as a Non-Executive Director and Chair of Remuneration Committee for both Mansfield Building Society and the Mortgage Advice Bureau. Rachel has a personal passion for ensuring customers are treated fairly and is particularly keen to make sure consumers, including those considered vulnerable, get value for money and good outcomes from their pension decisions. Rachel’s wide-ranging experiences will help the IGC build on its assessment of the value offered in both retirement products and investment pathways.

Steven joined the IGC as an Employee Member in September 2021. He is a qualified actuary who has been with the Phoenix Group for over 20 years with his current role being the Deputy Chief Actuary for the UK Life Companies for the Group, focused on overseeing the reserving calculations, managing risk, ensuring compliance with regulatory requirements, and developing strategic financial policies within the life companies of the group.

Steven joined the IGC as an Employee Member in September 2021. He is a qualified actuary who has been with the Phoenix Group for over 20 years with his current role being the Deputy Chief Actuary for the UK Life Companies for the Group, focused on overseeing the reserving calculations, managing risk, ensuring compliance with regulatory requirements, and developing strategic financial policies within the life companies of the group.

Steven’s previous roles at Phoenix have mainly been within the Actuarial team where he was responsible for pricing of new business for annuities and protection products, managing the Group’s exposure to longevity, mortality, expense, and persistency risks. He also has experience in developing the Group’s approach to determine the amount of regulatory capital required to be held given the type of business and risks the Group has on its books and also the workings and management of with-profits funds within the Group, and therefore has a broad experience across the business.

Andrew joined the IGC as an independent member in July 2022. He is an independent economist and investment consultant, who has 35 years' experience in financial markets, most notably at Aviva Investors as Head of Economic Research and Business Risk and then Aberdeen / Standard Life Investments as Head of Global Strategy. He currently has a portfolio of roles, including trustee to the Central Board of Finance, one of the three national bodies which handle the investments of the Church of England, sitting on the investment committee of the Health Foundation endowment, an investment adviser to the financial services company, and an Advisory Board member for the Devlin Mambo consultancy, especially concerned with ESG advice.

Andrew joined the IGC as an independent member in July 2022. He is an independent economist and investment consultant, who has 35 years' experience in financial markets, most notably at Aviva Investors as Head of Economic Research and Business Risk and then Aberdeen / Standard Life Investments as Head of Global Strategy. He currently has a portfolio of roles, including trustee to the Central Board of Finance, one of the three national bodies which handle the investments of the Church of England, sitting on the investment committee of the Health Foundation endowment, an investment adviser to the financial services company, and an Advisory Board member for the Devlin Mambo consultancy, especially concerned with ESG advice.

Maggie joined the IGC in January 2023. She spent all her executive career in the financial services industry. She has worked in the industry with Standard Life and Aegon, lobbied for the industry when at the Association of British Insurers and regulated the industry when at the FCA where she led pension policy during the pension freedom years and led the strategy for the FCA Scotland’s Office and set up the FCA Devolved Nations team. She was a Trustee on the Board of the FCA’s Pension Plan for two years. Alongside her day job at the FCA, Maggie regularly lectured on financial services regulation at Glasgow College and Heriot Watt University.

Maggie joined the IGC in January 2023. She spent all her executive career in the financial services industry. She has worked in the industry with Standard Life and Aegon, lobbied for the industry when at the Association of British Insurers and regulated the industry when at the FCA where she led pension policy during the pension freedom years and led the strategy for the FCA Scotland’s Office and set up the FCA Devolved Nations team. She was a Trustee on the Board of the FCA’s Pension Plan for two years. Alongside her day job at the FCA, Maggie regularly lectured on financial services regulation at Glasgow College and Heriot Watt University.

Maggie is Chair of Children 1st, Scotland’s national children’s charity, and sits on the Board of the Scottish Courts and Tribunal Service where she chairs the Audit and Risk Committee. She also sits on the Board of Glasgow Credit Union and is an honorary Fellow of the Institute and Faculty of Actuaries.

Maggie has been active on Diversity and Inclusion issues for several years with particular focus on mental health issues in part because she lives with a significant mental health condition.

Barry joined the IGC as an independent member in February 2025. He is a qualified actuary with over 35 years of experience in the insurance industry, most notably at MetLife as EMEA Head of Product, Underwriting & Sustainability, and Zurich as Global Head of Savings & Investment Propositions. He is an accomplished professional with extensive experience in products, customer propositions, risk management, sustainability, and cultural leadership. Currently he is a non-executive and consumer duty champion with MetLife, and a trustee and committee chair for Cotswold Lakes Trust. He is also studying for his Masters in Sustainable Development at the University of Sussex.

Barry joined the IGC as an independent member in February 2025. He is a qualified actuary with over 35 years of experience in the insurance industry, most notably at MetLife as EMEA Head of Product, Underwriting & Sustainability, and Zurich as Global Head of Savings & Investment Propositions. He is an accomplished professional with extensive experience in products, customer propositions, risk management, sustainability, and cultural leadership. Currently he is a non-executive and consumer duty champion with MetLife, and a trustee and committee chair for Cotswold Lakes Trust. He is also studying for his Masters in Sustainable Development at the University of Sussex.

Barry is passionate about the customer and will use his expertise in products, investments, and sustainability to support the IGC in ensuring customers get good value for money.

Previous reports

If you wish to read our previous reports they are available below:

IGC Interim Report January 2021 This report was produced after the IGC reporting timetable was changed from April to April to calendar year.

Old Mutual Wealth Life Assurance IGC Annual Report 2019/20 (This was the final report produced by the Old Mutual Wealth IGC. From the 2020 Report onwards, the IGC will take into account the former Old Mutual Wealth products and Scheme Members.)

Workplace pensions

Trustees of specific defined contribution (DC) occupational pension schemes, have to meet requirements on governance standards, charge controls and communications on pension flexibilities.

The requirements are detailed below:

- Appointing a chair of trustees who will sign an annual Chair’s statement

- Meeting certain governance standards and explaining this in the Chair’s statement, specifically:

- That core financial transactions are processed promptly and accurately

- That the value of charges and transaction costs borne by scheme members is reasonable

- That any default arrangements are designed in members’ interests and reviewed regularly

- That the Trustee board has the necessary knowledge and understanding to run the scheme properly

- Informing members about the increased range of options they have at retirement

ReAssure has two trustee boards, which you can read about below.

G Trustees Limited was established in 1986 and has been acting as trustee to a number of pension schemes administered by ReAssure since then. There are two directors who act solely in the interests of members, with any potential conflicts of interest considered in accordance with the Conflict of Interest policy, to ensure they can act independently of ReAssure. They look after;

- The ReAssure Number Three Executive Pension plan (with effect from 27 March 2018).

Trustees:

Paul worked in Management and Executive positions within the Operations (Customer Services and Information Technology) Division of ReAssure for more than 30 years. During that time he contributed towards the implementation of the key business administration and system strategies of the Company and played a key operational role in all Business Acquisitions and Migrations. He also served as Head of Business Solutions, where the focus was to guide the development of future strategies, systems and processes to support growth within the business and provide strong Customer outcomes.

Paul has a Bachelor’s degree in Economics and Accountancy from the University of Southampton.

Simon is the Chief Actuary for ReAssure and three other UK Life companies within the Phoenix Group. He is also the Chair of the Board of Namulas Pension Trustees Limited, a subsidiary of ReAssure, which acts as the Trustee of the National Mutual Personal Pension Scheme and the operator and administrator in relation to a further book of Self Invested Personal Pensions.

He is a qualified actuary with 35 years of experience in the UK Life market in a variety of actuarial and product development roles. He has previously served as a trustee of a defined benefits pension scheme and as a director of a local charity providing childcare for pre-school age children.

Grant is Head of Legal for Service, Integration and Group Operations within the Phoenix Group.

He is a qualified solicitor with over 15 years of experience in the financial services industry.

Prior to joining the Phoenix Group, Grant was a solicitor in the litigation team of a large multinational law firm.

ReAssure Trustees Limited no longer look after any active schemes. The below schemes have been wound up:

- Windsor Life Directors' Investment Programme

- National Pension Plan for Working Wives of General Practitioner Dentists